Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This is what happens when you respond to SPAM Email…

I am an avid TED Talks watcher and just came across this Talk. It's hysterical and I suspect will give you pause too! It's also hilarious!

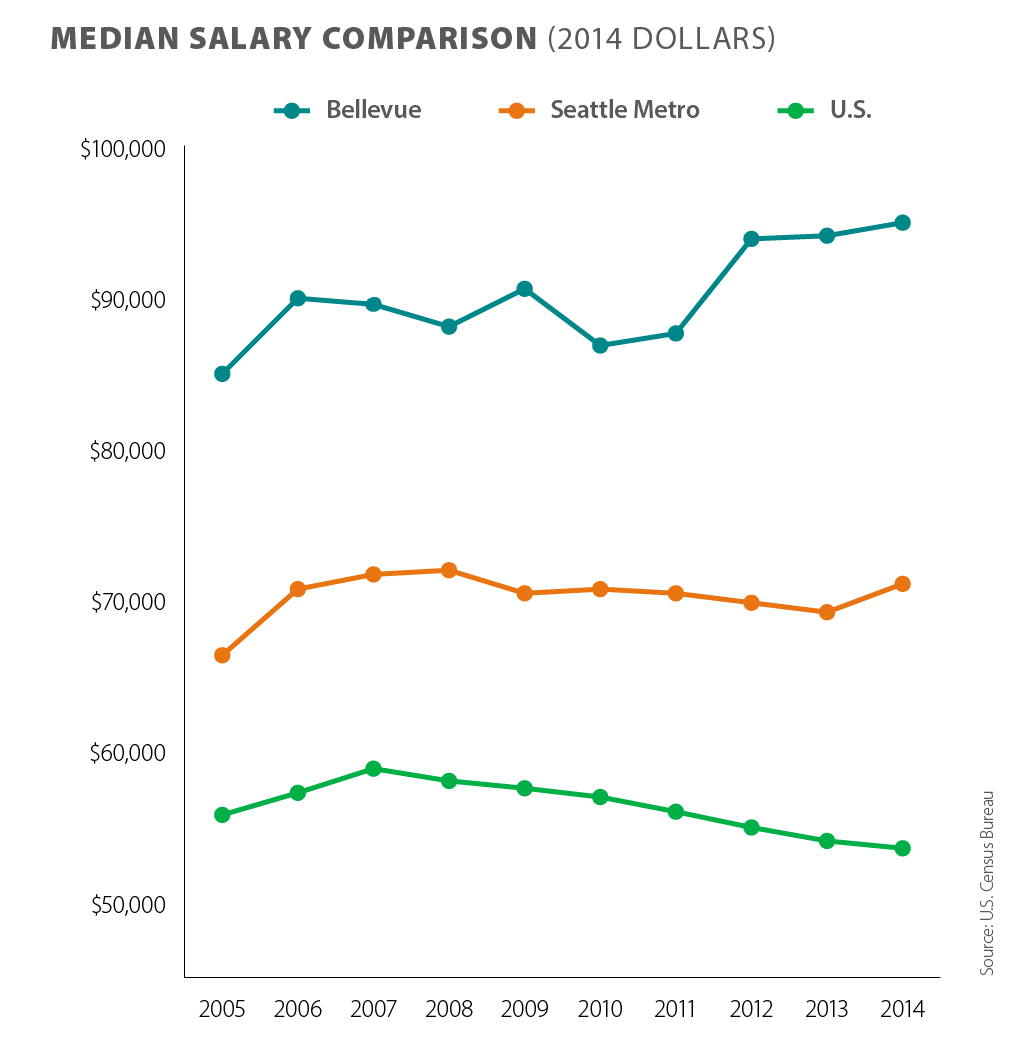

No Wage Stagnation on the Eastside

Wages on the Eastside are up

Last month’s U.S. Census report showed that middle-class incomes nationally were stagnant, confirming a trend that has been widely reported. But when 425Business magazine crunched the numbers for a local perspective, the picture changed. Unlike the U.S as a whole, median incomes in Bellevue and the greater Seattle area have risen – and wage growth has been particularly strong on the Eastside. A booming technology industry has made the Puget Sound area’s economic growth a standout.

Home prices soar as well

A steady influx of well-paid tech workers has boosted the local real estate market. With an increasing demand for homes, and not enough supply to meet the need, home prices have soared this year. The latest figures from the Northwest Multiple Listing Service show the median price of a single family home is up 10 percent over last year. If you’re considering selling, you’d be hard-pressed to find a better time to get top dollar for your home.

No Need To Panic About Rising Interest Rates

This article originally appeared on Inman.com

After seven years of some of the lowest interest rates in recorded history, the Federal Reserve has decided to raise the key Fed Funds Rate by 0.25 percent, which is causing some to be concerned that it will lead to a jump in mortgage rates and negatively impact the US housing market.

So, the question everyone wants to know is, do we need to worry about interest rates leaping?

While I expect there to be some volatility in rates for a while, I don’t believe the real estate market will implode in a rapidly rising interest rate environment. So, yes, interest rates are going to rise modestly, but no, I don’t think we need to be overly worried about it.

To qualify this statement, we need to understand that mortgage rates do not run in “lock-step” with the Fed Funds Rate. Although the Fed Funds Rate is a bellwether for the greater economic environment, there have been times when these two rates have moved in opposite directions, such as we saw in 2004/2005.

It’s also important to understand that while interest rates for revolving credit, such as credit cards and home equity loans, are tied to the Fed Funds Rate, non-revolving loans – like mortgages – are not. Mortgage rates are tied to bond yields – specifically the 10-year treasury.

So what do I think will happen?

I believe interest rates will rise above 4 percent, but we will not see a sharp spike in rates. The Fed has stated that any upward movement in the Fed Funds Rate will be slow and steady, and will reflect the greater economy. And I believe that mortgage rates will follow suit. Additionally, mortgage rates have already moved higher in anticipation of an increase in the Fed Funds Rate.

That said, it is worth noting that any weakness in the global economy can actually have a downward effect on interest rates. This is referred to a “flight to quality”. In essence, investors seek safe haven during times of economic uncertainty. If markets outside the U.S. continue to underperform, there will likely be increasing demand for bonds which will drive up their price and drive down interest rates. Between China, the Eurozone, war in the Middle East, and a massive drop in oil prices, it's certainly possible that the price of mortgage backed securities could rise, leading U.S. mortgage rates lower.

Interest rates could not realistically stay at their current levels forever. But an increase should not be a great cause for concern. Yes, an increase makes mortgages more expensive, but not to a point where they will have a negative effect on home values. That said, the rate of home price growth will undoubtedly slow in the coming year, but that isn’t necessarily a bad thing.

A little perspective might help: the average rate for a 30-year loan in the 1970’s was nine percent. It was 13 percent in the 1980’s and eight percent in the 1990’s. And yet people still managed to buy and sell homes throughout those years. With that in mind, the rate increases we’re likely to see in 2016 are nothing to fret over.

The increase in the Fed Funds Rate should be taken as a sign that our economy is expanding and is a preemptive move to limit anticipated inflation. While interest rates have risen from their all-time low, they are still remarkably favorable. And will remain so through 2016.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.