Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

6 Deck Renovations That Really Pay Off—and 1 That Doesn’t

Charles Schmidt/iStock

If there’s one thing that unites this great country—especially once the weather starts getting warmer and barbecue season gets ever so tantalizingly closer—it is our passionate, even obsessive love for our outdoor decks. Truth be told, just about all of us desire a perch from which to survey our backyard (or rooftop) kingdom, lazily hang out, or busily entertain.

One story behind the origin of decks is that they were inspired by boat decking. But unlike new yawls or yachts—which will depreciate in value by an average of 24% in just three years—a brand-new wooden deck addition to your home will net you a 75% return on investment when you decide to sell, according to Remodeling Magazine’s 2016 Cost vs. Value Report.

That’s why in honor of summer’s sweet approach, we take a look at the ROI for decks in our latest installment of Renovations That Really Pay Off. Whether you are building one from scratch or just want to make the one you have bigger and better, here’s how to get your deck on this summer in ways that will pay off awesomely down the road.

Gratis guidance

Before you pick up a hammer, review the wildly useful free deck guide from the American Wood Council. Did we mention it’s free? Here you’ll find safe construction specs so you can get your rim joists and ledger boards just so. This should also be when you decide on deck size—a 200-square-foot deck will run you about $4,836—keeping in mind an addition could jack up your property taxes and insurance. Getting those hard numbers will help you figure out your overall budget (handy deck cost calculator here).

Getting started

The average contractor charges $35 per square foot to build a deck, but where the cost can vary enormously is in the material. Hollow-core PVC can cost as little as $7.50 per square foot, cedar even less at $3.50—while the Brazilian hardwood ipe goes for a nosebleed-inducing $22 or more (compare prices here).

A great way to save money? “Design your deck for standard lengths of lumber: 6-, 8-, 10-, or 12-foot boards,” says Chris Peterson, author of “Deck Ideas You Can Use.” This will eliminate any wasted wood from cutoffs. Peterson also suggests buying secondhand. “Organizations like Habitat for Humanity sell reclaimed wood from demos, as do some local salvage shops.” In addition to possibly scoring unique hardwoods, “the savings can be significant.”

Protect your investment

Your deck is constantly exposed to sun, rain, snow, and the occasional melted Creamsicle. Peterson advises “waterproofing wood decks regularly to ensure longevity … even if you’re letting the cedar or redwood age naturally. Water can cause direct damage in the form of rot and indirect damage like mold.”

Harry Adler of Adler’s Design Center & Hardware in Providence, RI, recommends protecting vulnerable surfaces with a product such as C2 Guard, a nontoxic waterproofer designed for use on unsealed wood and concrete surfaces.

Beyond wood

Pure, quality wood is the gold standard for decks. But there are other options, according to Bill Leys, aka The Deck Expert.

“Wood decks need yearly maintenance, and those costs can rapidly add up over the 20 years they’re expected to last,” Leys says.

James Brueton of EnviroBuild recommends using a quality wood composite, “which initially has a slightly higher cost. But without the need to treat the deck every year, you’re soon saving money over traditional wood.”

TimberTech is the only premium wood composite decking that is capped with a protective polymer on all four sides. Better yet, all TimberTech decking comes with a 25-year limited residential warranty.

Eye on entertaining

Outdoor entertaining should be the key focus of any deck design, Brueton says.

“Especially when reselling your home, any new buyer will immediately see the appeal of barbecue days and summer nights” on a deck, he says. Since all these revelers will need a place to sit, one easy way to add that is a built-in bench made out of the same wood as the deck itself. It generally offers a strong ROI.

This look is not only streamlined but also relatively budget-friendly, costing $500 to $1,500, says J.B. Sassano, president of Mr. Handyman, a national home improvement franchise. Best of all, such seats will withstand the elements as well as the flooring underneath.

That said, don’t throw style and comfort under the bus. Make sure to add cushions and choose at least one statement piece of furniture with a “pop of color to reflect your personality and design taste,” suggests Sassano. Like this bright yellow chair for $140.

Light the way

If you plan to hang out on your deck well after sunset, fireflies aren’t going to cut it as a light source. Modernize—a website that empowers homeowners to get home improvement projects done—suggests simple ground lights ($28 each) to stringing fairy lights (starting at $15) to solar lights.

Don’t play with fire

Built-in or portable fire pits are warm, cozy, and “the source of deck fires. Whether embers blow out of the pit or the heat from the pit ignites the wood deck, the result is often tragic, with homes burned to the ground,” says Leys. Er, not such a great ROI. Place your fire pit in the backyard far from anything flammable. And to safely heat things up on your deck, buy a patio warmer ($150 to $400) says Sassano.

—————-

This article originally appeared on Realtor.com

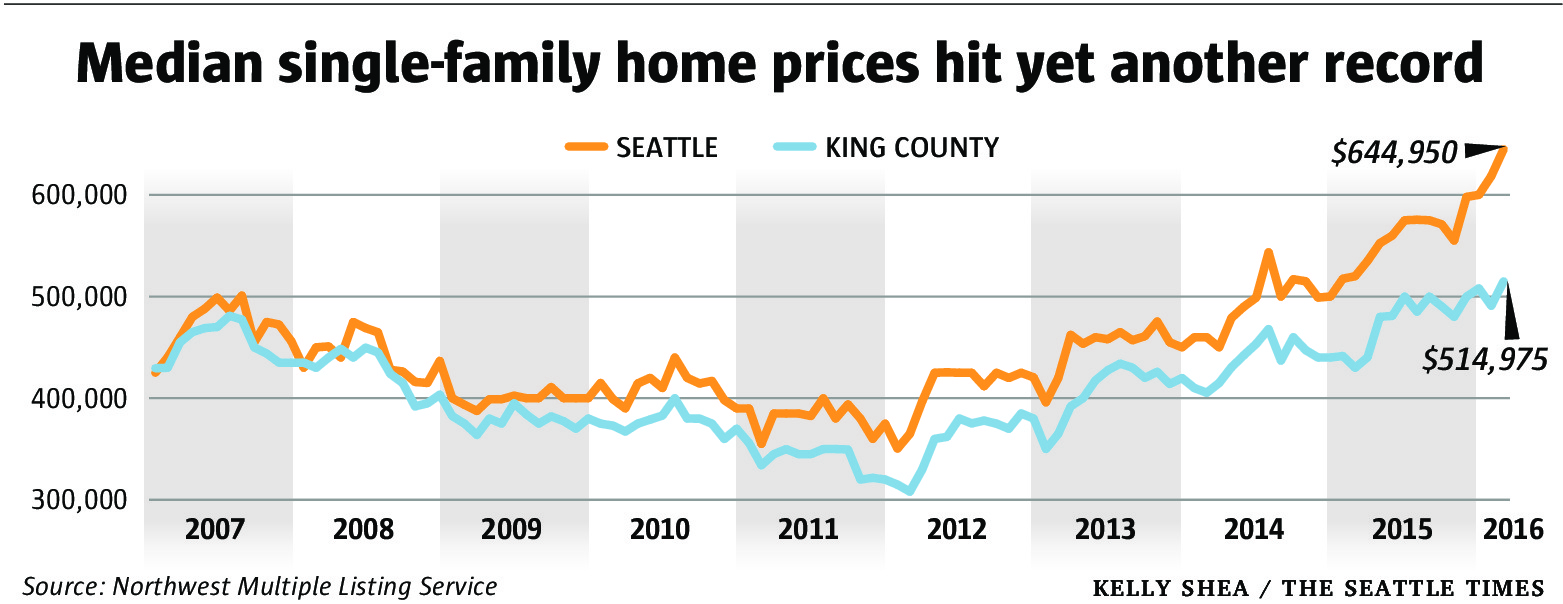

Scarce listings drive King County home prices to new highs

The median price of single-family homes sold in King County hit a new all-time high last month — $514,975 — amid record-low inventory, heralding even more intense bidding wars ahead in the typically busy spring home-buying season.

Ominously, the more affordable Snohomish and Pierce counties also face a historically low inventory level, according to a Seattle Times analysis of data from the Northwest Multiple Listing Service.

One widely-watched gauge of supply — the ratio of active listings to pending sales — hit its lowest level since at least 2003 in all three counties in February, according to the Times’ analysis. King and Snohomish counties each had less than a month’s supply, while Pierce had just over a month’s supply.

The historic shortage of homes for sale, combined with a recent drop in interest rates, has caused the dramatic run-up in prices, experts say. In February, King County had 1,923 homes listed for sale, the MLS reported, but a greater number of pending sales that hadn’t yet closed: 2,299.

“We cannot continue to sell more homes than we list,” said Matthew Gardner, chief economist at Windermere Real Estate. “When are we going to start seeing some listings? That scares me more than anything else.”

Single-family home prices in the city of Seattle jumped 24 percent over the year to a median $644,950. Despite an older housing stock, Seattle is ground-zero for the region’s job growth.

Expedia and Weyerhaeuser are moving their suburban headquarters to Seattle. Amazon.com recently opened its new high-rise campus in South Lake Union. And Silicon Valley titans like Facebook and Apple have established satellite offices here.

This article originally appeared in the Seattle Times. To read more, click here.

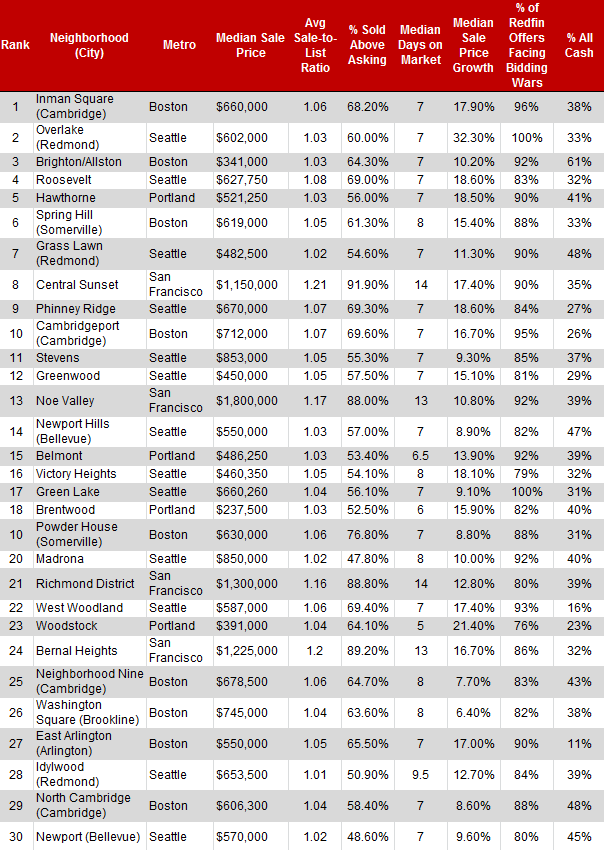

King County Had Almost Half of 2015’s 30 Most Competitive Neighborhoods in America

We probably don’t need to tell you that 2015 was a crazy year in real estate, especially in our city. Bidding wars and listings lasting mere days on the market is something we’ve all grown accustomed to. But it turns out we’re not alone. Redfin recently came out with a list of the 30 most competitive neighborhoods from all across the U.S.. What’s the most mind blowing thing about this list? Of the 30 neighborhoods listed, 13 of them are in King County.

Seattle neighborhoods that made it onto this list are Roosevelt (4th), Phinney Ridge (9th), Stevens (11th), Greenwood (12th), Victory Heights (16th),Green Lake (17th), Madrona (20th), West Woodland (22nd). I mean, we all knew it was stormy out there, but this felt like a snow storm in Waikiki. It’s hard to say exactly what 2016 has in store, but our very own Chief Economist, Matthew Gardner, has a few ideas (such as expecting that housing in Seattle will continue to appreciate in value, but at a slightly lower rate than 2015).

Read more on Seattle Curbed.

This article originally published on Windermere Seattle's blog.

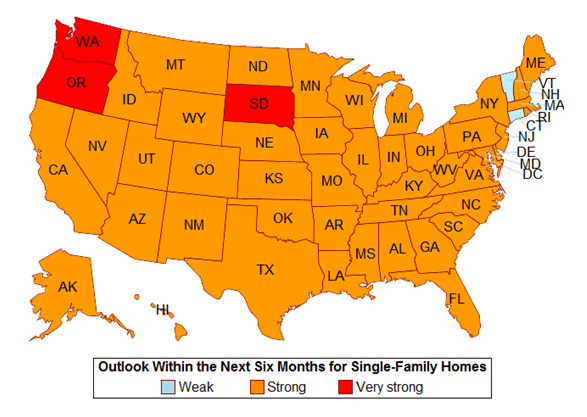

2016 Housing Forecast: “Very Strong” for Sellers

According to a recent REALTORS® Confidence Index Survey Report, 2016 is projected to be a very strong market for local area sellers.

With inventory at historic lows, prices at or near record highs, and multiple offers the norm, it’s an exceptional time to get top dollar for your home.

Washington is one of only three states in the country projecting a “very strong” market for single family home sales.

This information was originally posted on Windermere Eastside's blog. Read more here!

This is what happens when you respond to SPAM Email…

I am an avid TED Talks watcher and just came across this Talk. It's hysterical and I suspect will give you pause too! It's also hilarious!

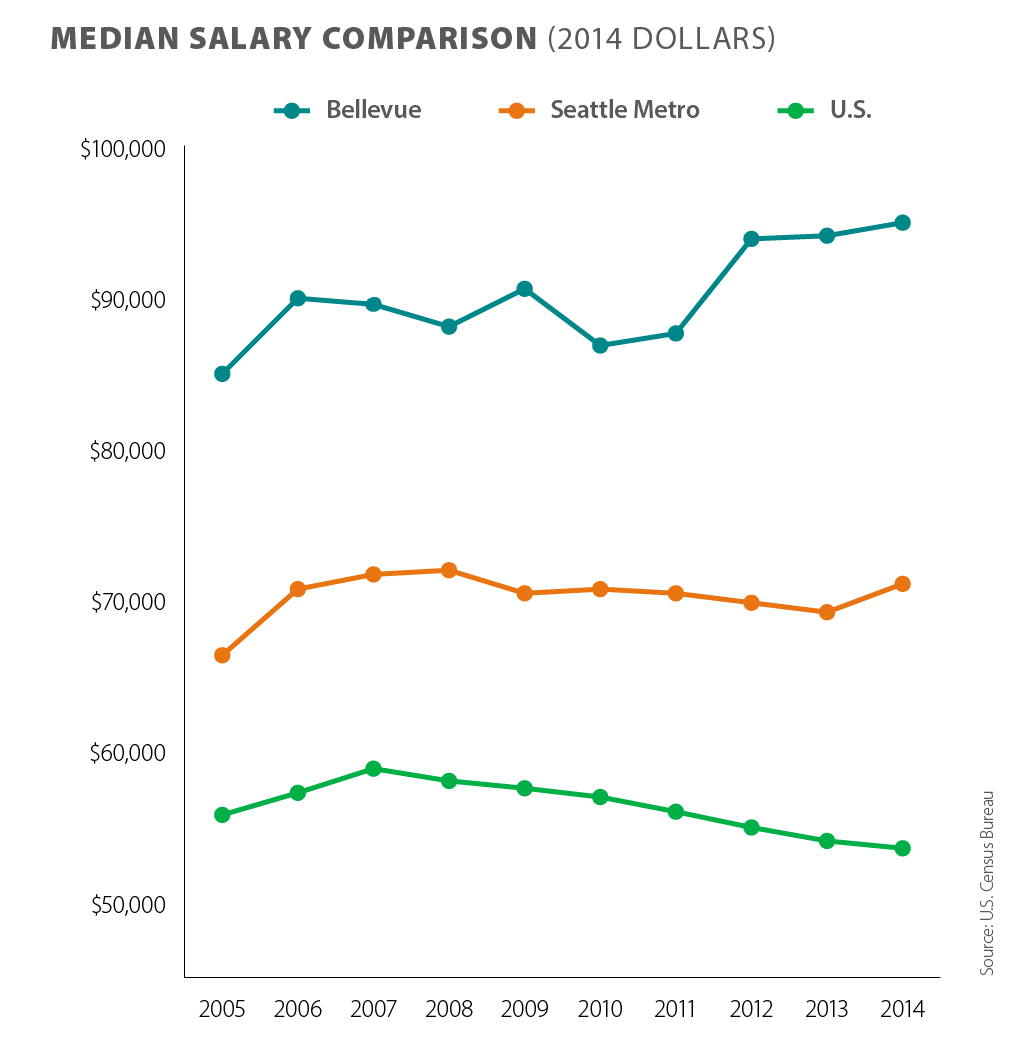

No Wage Stagnation on the Eastside

Wages on the Eastside are up

Last month’s U.S. Census report showed that middle-class incomes nationally were stagnant, confirming a trend that has been widely reported. But when 425Business magazine crunched the numbers for a local perspective, the picture changed. Unlike the U.S as a whole, median incomes in Bellevue and the greater Seattle area have risen – and wage growth has been particularly strong on the Eastside. A booming technology industry has made the Puget Sound area’s economic growth a standout.

Home prices soar as well

A steady influx of well-paid tech workers has boosted the local real estate market. With an increasing demand for homes, and not enough supply to meet the need, home prices have soared this year. The latest figures from the Northwest Multiple Listing Service show the median price of a single family home is up 10 percent over last year. If you’re considering selling, you’d be hard-pressed to find a better time to get top dollar for your home.

No Need To Panic About Rising Interest Rates

This article originally appeared on Inman.com

After seven years of some of the lowest interest rates in recorded history, the Federal Reserve has decided to raise the key Fed Funds Rate by 0.25 percent, which is causing some to be concerned that it will lead to a jump in mortgage rates and negatively impact the US housing market.

So, the question everyone wants to know is, do we need to worry about interest rates leaping?

While I expect there to be some volatility in rates for a while, I don’t believe the real estate market will implode in a rapidly rising interest rate environment. So, yes, interest rates are going to rise modestly, but no, I don’t think we need to be overly worried about it.

To qualify this statement, we need to understand that mortgage rates do not run in “lock-step” with the Fed Funds Rate. Although the Fed Funds Rate is a bellwether for the greater economic environment, there have been times when these two rates have moved in opposite directions, such as we saw in 2004/2005.

It’s also important to understand that while interest rates for revolving credit, such as credit cards and home equity loans, are tied to the Fed Funds Rate, non-revolving loans – like mortgages – are not. Mortgage rates are tied to bond yields – specifically the 10-year treasury.

So what do I think will happen?

I believe interest rates will rise above 4 percent, but we will not see a sharp spike in rates. The Fed has stated that any upward movement in the Fed Funds Rate will be slow and steady, and will reflect the greater economy. And I believe that mortgage rates will follow suit. Additionally, mortgage rates have already moved higher in anticipation of an increase in the Fed Funds Rate.

That said, it is worth noting that any weakness in the global economy can actually have a downward effect on interest rates. This is referred to a “flight to quality”. In essence, investors seek safe haven during times of economic uncertainty. If markets outside the U.S. continue to underperform, there will likely be increasing demand for bonds which will drive up their price and drive down interest rates. Between China, the Eurozone, war in the Middle East, and a massive drop in oil prices, it's certainly possible that the price of mortgage backed securities could rise, leading U.S. mortgage rates lower.

Interest rates could not realistically stay at their current levels forever. But an increase should not be a great cause for concern. Yes, an increase makes mortgages more expensive, but not to a point where they will have a negative effect on home values. That said, the rate of home price growth will undoubtedly slow in the coming year, but that isn’t necessarily a bad thing.

A little perspective might help: the average rate for a 30-year loan in the 1970’s was nine percent. It was 13 percent in the 1980’s and eight percent in the 1990’s. And yet people still managed to buy and sell homes throughout those years. With that in mind, the rate increases we’re likely to see in 2016 are nothing to fret over.

The increase in the Fed Funds Rate should be taken as a sign that our economy is expanding and is a preemptive move to limit anticipated inflation. While interest rates have risen from their all-time low, they are still remarkably favorable. And will remain so through 2016.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.